The ongoing commercial real estate crisis is becoming a significant concern for the U.S. economy as high office vacancy rates continue to plague major cities. With reported vacancy levels ranging from 12% to 23%, many property values are in jeopardy, particularly as deadlines for real estate loans loom in the coming years. Economic downturns and rising interest rates exacerbate the situation, sparking fears of widespread financial distress within the banking system. Kenneth Rogoff, an economic expert, highlights the potential repercussions of increased delinquencies among commercial real estate loans, which could rattle other economic sectors and lead to bank failures. As we navigate this challenging landscape, understanding the interconnectedness of these factors is crucial to grasping the future of the market and its broader implications.

As we delve into the current challenges facing the sector of commercial properties, many experts voice concerns over the implications of high vacancy rates in office spaces. This situation, intertwined with a potential banking system impact due to looming debts, signals an urgent need for analysis. Investors and stakeholders must remain cognizant of the fragility of real estate loans amidst a struggling economic landscape. Kenneth Rogoff’s insights shed light on how this sector may influence broader economic outcomes, especially as financial institutions brace for the wave of debt maturing soon. Understanding these dynamics is essential as we explore the intricacies of commercial property market trends and their effects on both local economies and the financial system at large.

Understanding Commercial Real Estate Crisis

The commercial real estate crisis is looming large, characterized by high office vacancy rates and mounting concerns over significant delinquencies on loans. As remote working reshapes the landscape of urban office spaces, many businesses have downsized or withdrawn from brick-and-mortar operations entirely, leading to vacancy rates that have skyrocketed to alarming levels. In cities like Boston, vacancy rates range between 12% to 23%, creating a ripple effect on property values and alarming investors across the board.

Kenneth Rogoff, an expert on economic predictions, warns that the consequences of this crisis could severely impact the banking system in the coming years. The $4.7 trillion in commercial mortgage debt, of which a significant portion—20%—is due this year, could potentially lead to a wave of financial distress if not managed appropriately. As firms face massive losses and some may see their equity wiped out, the specter of a crisis similar to that of 2008 still lingers in discussions among financial analysts.

The Impact of Office Vacancy Rates on the Economy

High office vacancy rates directly correlate with broader economic implications. With a decline in demand for traditional office spaces, there is a concomitant decrease in property values, meaning that landlords and real estate investors are facing significant losses. This decline in asset values, when coupled with rising interest rates by the Federal Reserve, creates a challenging environment not only for property owners but also for banks that provided financing for these assets.

Moreover, the geographic concentration of these vacancies, particularly in major U.S. cities, could lead to regional economic imbalances. If a significant portion of commercial real estate operates at a loss, it could trigger tighter lending conditions from banks, further stifling local economies through reduced consumption and spending. As Kenneth Rogoff points out, while some key indicators like the job market remain strong, the stability of the economy seems precarious, hinging on the performance of sectors like commercial real estate.

Banking System Vulnerability and Real Estate Loans

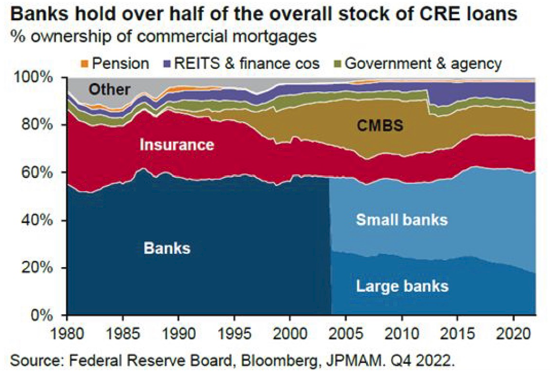

The interconnectedness of commercial real estate loans and the banking system raises alarms about possible vulnerabilities. Smaller banks that are heavily reliant on commercial real estate may find themselves facing significant pressures if these loans turn delinquent. Kenneth Rogoff highlights that while most large banks could weather the storm due to stricter regulations post-2008, regional banks may not be as insulated, risking exposure to losses that could ripple throughout the banking sector.

As interest rates rise and property values decline, these smaller banks may struggle to meet their capital requirements, potentially leading to a situation where a few failures could cascade into larger market disruptions. This scenario emphasizes the critical importance of regulatory foresight in mitigating risk within the financial system, as the intertwining fates of banks and commercial real estate standardize some systemic vulnerabilities.

Kenneth Rogoff’s Insights on Economic Downturn

Kenneth Rogoff’s insights into the economic landscape provide an essential lens through which we can analyze the potential fallout from the current crisis. He suggests a cautious optimism; despite the looming commercial real estate crisis, a full-blown financial meltdown like that seen in 2008 is unlikely under current conditions. Rogoff stresses that strong underlying economic fundamentals, including a robust job market and rising consumer confidence, could cushion the impact of commercial losses.

However, Rogoff is also acutely aware of the risks posed by rising delinquency rates on commercial loans. He notes that while larger financial institutions have managed to maintain profitability through diversified portfolios and revenue-generation strategies, the exposure of regional banks to commercial real estate could still spell trouble. Therefore, sustaining vigilance while navigating these waters remains a critical priority for stakeholders as the economic landscape evolves.

Strategies to Mitigate Commercial Real Estate Crisis

To mitigate the consequences of the commercial real estate crisis, some experts suggest policy adjustments to address both the high vacancy rates and the ensuing financial strain on banks. There could be a concerted effort to reduce interest rates strategically to incentivize borrowing and investment in commercial properties. If long-term rates fall, property owners could refinance their loans, allowing them to adjust without severe financial burdens.

Another proposed strategy is to repurpose or redevelop vacant office spaces into residential units or mixed-use properties. Although logistical challenges abound in converting these spaces due to structural drawbacks, addressing zoning issues and providing incentives for transformation can revitalize struggling commercial areas and stimulate economic growth, which would be vital during these challenging times.

Economic Distress and Consumer Implications

The current crisis in commercial real estate will inevitably trickle down to consumers, albeit indirectly at first. If regional banks suffer substantial losses due to heavy investment in delinquent commercial loans, this could result in restrictive lending practices that impact consumers’ ability to access credit. It may also lead to broader economic distress in the regions most affected, dampening consumer confidence and spending.

Furthermore, as pension funds, which often hold significant investments in commercial real estate, face losses, consumers reliant on these funds will feel the pinch, potentially jeopardizing their savings and future financial stability. Despite the strong job market, the paradox remains: sections of the economy may thrive while another sector suffers a downturn. If a major recession were to ensue, the implications for consumers could be far-reaching, amplifying the challenges posed by the commercial real estate crisis.

Potential Long-Term Outlook for Commercial Real Estate

The long-term outlook for commercial real estate hinges on several factors, including policy decisions regarding interest rates and economic recovery strategies implemented post-crisis. Kenneth Rogoff posits that interest rates might eventually stabilize, potentially allowing for a recovery in the commercial property market, with the hope that demand for office space will rebound as businesses adapt to new work models. Investors remain hopeful that conditions will improve before the significant wave of debt matures.

However, investors should brace for a bumpy road ahead. The distressed nature of the office space segment will not resolve overnight, and many investors might need to maintain a longer investment horizon to see returns. Those heavily invested in the sector must evaluate their risk tolerance and strategize accordingly to navigate through this unpredictable landscape and mitigate potential losses.

Reforming Policy for a Resilient Economy

Reforming financial policies to enhance resilience in the commercial real estate sector is critical as the economy navigates the current crisis. Policymakers could introduce measures that promote transparent assessments of asset values and strengthen capital requirements for banks heavily engaged in commercial real estate lending. This transparency fosters a robust banking environment that can better withstand shocks brought about by economic downturns.

Additionally, initiatives aimed at economic diversification could relieve pressure on commercial real estate markets by encouraging alternative developments that generate demand for office space. Community investments that foster innovation and support local businesses can yield growth opportunities that counterbalance the existing risks in the commercial real estate sector, paving the way for long-term stability.

Understanding the Role of Larger Banks in Crisis Management

In a crisis context, larger banks play a pivotal role in managing a potential cascade of bad debts within the commercial real estate sector. Given their diversified portfolios and stronger capital base, institutions like JPMorgan Chase and Bank of America are generally better positioned to absorb shocks from defaulting loans, compared to smaller competitors. Their substantial profits derived from various sectors provide them with a buffer against the adverse impacts of commercial real estate downturns.

However, the interconnectedness of these larger banks with regional institutions amplifies the need for cooperative strategies to uphold financial stability across the board. As Kenneth Rogoff indicates, ensuring that the larger financial institutions continue to prosper while engaging in prudent lending practices is crucial, as their performance has significant ripple effects on the broader economy and smaller banks.

Frequently Asked Questions

What is the connection between high office vacancy rates and the commercial real estate crisis?

High office vacancy rates are a significant factor contributing to the commercial real estate crisis. As businesses adopt remote and hybrid work models, demand for office space has dropped, leading to vacancy rates as high as 23% in major U.S. cities. This oversupply depresses property values and affects the viability of real estate loans associated with these properties, further exacerbating the crisis.

How does the commercial real estate crisis impact the banking system?

The commercial real estate crisis poses risks to the banking system as a large portion of real estate loans are coming due. If delinquencies increase among these loans, especially at smaller and regional banks, it could lead to significant losses and potentially some bank failures. The interconnected nature of these loans means issues within commercial real estate can ripple through the banking sector.

What role do economic downturns play in the commercial real estate crisis?

Economic downturns significantly aggravate the commercial real estate crisis by reducing demand for office space and increasing vacancy rates. As companies scale back operations or adopt remote work, the likelihood of default on real estate loans rises, further straining the market and leading to decreased property values, which can negatively impact the overall economy.

What insights has Kenneth Rogoff provided regarding the commercial real estate crisis?

Kenneth Rogoff has warned that while the commercial real estate crisis could lead to significant losses for investors and banks, it is not expected to trigger a full-blown financial crisis like in 2008. His insights highlight the potential for regional banks to experience distress due to their exposure to commercial real estate loans, but he believes that larger banks are better positioned to withstand these challenges.

Why are some experts concerned about the wave of commercial real estate loans maturing soon?

Experts are worried about the wave of commercial real estate loans maturing soon, as approximately 20% of U.S. commercial mortgage debt comes due this year. Rising interest rates combined with high vacancy rates mean that many properties may not generate sufficient income to cover debt obligations, leading to increased delinquencies and financial instability within the lending community.

How could high vacancy rates in commercial real estate affect consumers?

High vacancy rates in commercial real estate can lead to reduced property values and, consequently, affect pension funds and investments of ordinary consumers. Losses in this sector may restrict lending by regional banks, further constraining consumer spending. However, the overall economic impact may be mitigated by a strong job market, depending on how widespread the fallout from the crisis becomes.

What immediate actions could mitigate the impact of the commercial real estate crisis?

Mitigating the impact of the commercial real estate crisis may require significant intervention, such as reductions in long-term interest rates to facilitate refinancing. Additionally, there could be a need for policy adjustments to support distressed loans or encourage adaptive reuse of commercial properties. However, without these measures, the cycle of bankruptcies and loan defaults may continue affecting the economy.

How does commercial real estate crisis compare to the financial crisis of 2008?

The current commercial real estate crisis is viewed as a ‘slow-moving train wreck’ which, while serious, differs from the abrupt financial crisis of 2008. The regulatory environment for banks has tightened since 2008, providing some safeguards against widespread failures. Although significant losses are expected in commercial real estate, experts like Kenneth Rogoff suggest that it may not lead to a systemic collapse as seen in the previous crisis.

| Key Point | Details |

|---|---|

| High Office Vacancy Rates | Vacancy rates in major cities range from 12% to 23% due to a decline in demand for office space post-pandemic. |

| Commercial Mortgage Debt | 20% of the $4.7 trillion commercial mortgage debt is due this year, posing risks for banks and investors. |

| Bank Stability Risks | Small to medium banks may face difficulties due to over-leveraged investments in commercial real estate. |

| Impact of Interest Rates | High interest rates have pressured commercial real estate investments, complicating refinancing options. |

| Potential Economic Impact | Losses in commercial real estate may lead to tighter lending and reduced consumer spending, despite a strong economy overall. |

| Long-term Property Adaptation Issues | Converting vacant office spaces into apartments is complicated due to zoning and engineering challenges. |

| GFIs Preparedness | Large banks are more diversified and profitable in other sectors, reducing the risk of a full-blown financial crisis. |

Summary

The commercial real estate crisis is a significant concern for the economy in 2024, particularly as high office vacancy rates and substantial commercial mortgage debt converge. While the current economic backdrop remains relatively strong, the looming risks associated with delinquent loans and the potential for regional bank failures highlight the fragility of this sector. With a considerable percentage of commercial mortgages coming due, businesses and investors must navigate a complex landscape marked by rising interest rates and declining property values. Overall, while immediate financial catastrophes may be averted, vigilant monitoring and strategic adjustments will be crucial as we move forward.